Terry & Nancy's Ancestors

Family History Section

Person Page 1,898

Rachel Clara Shurtz1,2,3

#18971, (1863 - 1954)

Parents

| Father | Frederick J. Shurtz (1832 - 18 May 1892) |

| Mother | Margaret Ann Derr (14 May 1829 - 18 Sep 1865) |

| Family Indexes | The Reigel Family |

Key Events:

Copyright Notice

The material on this website is subject to copyright.

Facts – names, dates, and places – cannot be copyrighted; you are free to copy them.

But the narratives are my creative work product and are copyrighted. You may copy them for your personal use, but please respect my copyright and do not republish them in any form, including copying them to your tree on Ancestry or elsewhere, unless you have obtained written permission from me.

Many of the images are also copyrighted, and may not be copied without the consent of the copyright holders.

Narrative:

Rachel Clara Shurtz was born on 23 Feb 1863 in Lewis Twp., Northumberland Co., PennsylvaniaG.4,5,6

She generally used her middle name, Clara, rather than her first name.2,15,16

She moved to St. Joseph Co., MichiganG, Circa 1864 with her parents, Frederick J. Shurtz and Margaret Ann Derr.17

Her mother died on 18 Sep 1865, when Clara was 2 years old.18,19 Clara appeared on the 1870 Federal Census of Centerville, St. Joseph Co., MichiganG, in the household of her father and stepmother, Sarah Elizabeth Riegel.20

Clara moved to IowaG with her father and stepmother Circa 1880. She appeared on the 1880 Federal Census of Fisher Twp., Fremont Co., Iowa G, in the household of her father, and stepmother.21 She appeared on the 1885 State Census of Shenandoah, Page Co., IowaG, in the household of her father and stepmother.22

She was a teacher before her marriage.22

Rachel married Hartley J. Setchell, son of Hartley Setchell and Amanda J., Circa 1893.7,8,9

Clara and Hartley moved to KansasG after their marriage. They appeared on the 1900 Federal Census of Logan, Phillips Co., Kansas G, enumerated 1 Jun 1900, reporting that they owned their home. Their children Fern and Fred and his children by his previous marriage, Hartley and Clara, were listed as living with them.23

Clara and Hartley appeared on the 1910 Federal Census of Soloman, Graham Co., Kansas G, enumerated 3 May 1910, reporting that they owned their home. Their children Fern and Fred were listed as living with them, as wer his children Hartley and Clara.24 They appeared on the 1915 State Census of Soloman, Graham Co., KansasG, reporting that they owned their home. Their son Fred was listed as living with them as were his children Hartley and Clara.25

Clara and Hartley appeared on the 1920 Federal Census of Soloman, Graham Co., Kansas G, enumerated 25 Jan 1920, reporting that they owned their home. Their son Fred and his son Hartley were listed as living with them.26 They appeared on the 1925 State Census of Soloman, Graham Co., KansasG, reporting that they owned their home.27

Her husband died Between 1925 and 1930.28,29

Clara appeared on the 1930 Federal Census of Soloman, Graham Co., Kansas G, enumerated 22 Apr 1930, with her step-daughter Clara was listed with her and shown as owner of the home. Also listed were Robert DeNune and Charles Bourland, farm laborers, described as lodgers.30 Clara appears to have taken over operation of the family farm after the death of her husband.31

By 1931 Clara moved to Denver, Colorado, to live with her daughter, at 5524 Montview.32 Clara appeared on the 1940 Federal Census of Denver, Colorado G, in the household of Fern and Roy D. Slagle, her daughter and her husband, at 2450 Julian St. She reported she had lived in the same city in 1935.33

By 1945 they had moved to 1723 Vine, Apt. 1-2G, where she lived with them until at least 1951.34

Rachel appeared on the 1950 Federal Census of Denver, Colorado, G in the household of her daughter Fern and her husband, Roy D. Slagle.35

Rachel died on 1 Nov 1954 at age 91.10,11,12 She was buried on 2 Nov 1954 in Crown Hill Cemetery, Wheat Ridge, Jefferson Co., ColoradoG.13,14

She generally used her middle name, Clara, rather than her first name.2,15,16

She moved to St. Joseph Co., MichiganG, Circa 1864 with her parents, Frederick J. Shurtz and Margaret Ann Derr.17

Her mother died on 18 Sep 1865, when Clara was 2 years old.18,19 Clara appeared on the 1870 Federal Census of Centerville, St. Joseph Co., MichiganG, in the household of her father and stepmother, Sarah Elizabeth Riegel.20

Clara moved to IowaG with her father and stepmother Circa 1880. She appeared on the 1880 Federal Census of Fisher Twp., Fremont Co., Iowa G, in the household of her father, and stepmother.21 She appeared on the 1885 State Census of Shenandoah, Page Co., IowaG, in the household of her father and stepmother.22

She was a teacher before her marriage.22

Rachel married Hartley J. Setchell, son of Hartley Setchell and Amanda J., Circa 1893.7,8,9

Clara and Hartley moved to KansasG after their marriage. They appeared on the 1900 Federal Census of Logan, Phillips Co., Kansas G, enumerated 1 Jun 1900, reporting that they owned their home. Their children Fern and Fred and his children by his previous marriage, Hartley and Clara, were listed as living with them.23

Clara and Hartley appeared on the 1910 Federal Census of Soloman, Graham Co., Kansas G, enumerated 3 May 1910, reporting that they owned their home. Their children Fern and Fred were listed as living with them, as wer his children Hartley and Clara.24 They appeared on the 1915 State Census of Soloman, Graham Co., KansasG, reporting that they owned their home. Their son Fred was listed as living with them as were his children Hartley and Clara.25

Clara and Hartley appeared on the 1920 Federal Census of Soloman, Graham Co., Kansas G, enumerated 25 Jan 1920, reporting that they owned their home. Their son Fred and his son Hartley were listed as living with them.26 They appeared on the 1925 State Census of Soloman, Graham Co., KansasG, reporting that they owned their home.27

Her husband died Between 1925 and 1930.28,29

Clara appeared on the 1930 Federal Census of Soloman, Graham Co., Kansas G, enumerated 22 Apr 1930, with her step-daughter Clara was listed with her and shown as owner of the home. Also listed were Robert DeNune and Charles Bourland, farm laborers, described as lodgers.30 Clara appears to have taken over operation of the family farm after the death of her husband.31

By 1931 Clara moved to Denver, Colorado, to live with her daughter, at 5524 Montview.32 Clara appeared on the 1940 Federal Census of Denver, Colorado G, in the household of Fern and Roy D. Slagle, her daughter and her husband, at 2450 Julian St. She reported she had lived in the same city in 1935.33

By 1945 they had moved to 1723 Vine, Apt. 1-2G, where she lived with them until at least 1951.34

Rachel appeared on the 1950 Federal Census of Denver, Colorado, G in the household of her daughter Fern and her husband, Roy D. Slagle.35

Rachel died on 1 Nov 1954 at age 91.10,11,12 She was buried on 2 Nov 1954 in Crown Hill Cemetery, Wheat Ridge, Jefferson Co., ColoradoG.13,14

Children:

Children with Hartley J. Setchell:

- Clara L. V. Setchell (28 Nov 1889 - Dec 1974)

- Fern E. Setchell (14 Sep 1894 - Jul 1973)

- Fred M. Setchell (20 Dec 1899 - 4 Feb 1977)

Citations

- [S4985] Cochrane, Family File "Margaret Ann Derr family," 24 Oct 2014, shows name as Rachel Clara (Cora) Shurtz.

- [S4754] F. Shurtz household, 1880 U.S. Census, Fremont Co., Iowa, shows name as Clara Shurtz.

- [S4755] Frederick Shurtz household, 1885 Iowa State Census, Page Co., Iowa, Shenandoah, shows name as Rachel C. Shurtz.

- [S4985] Cochrane, Family File "Margaret Ann Derr family," 24 Oct 2014, shows date, township, county, and state.

- [S4753] Frederick Shortz household, 1870 U.S. Census, St. Joseph Co., Michigan, shows age 7 and state.

- [S5017] Hartley J. Setchell household, 1900 U.S. Census, Phillips Co., Kansas, shows month, year, age 37, and state.

- [S5017] Hartley J. Setchell household, 1900 U.S. Census, Phillips Co., Kansas, shows married 7 years.

- [S5018] H. J. Setchell household, 1910 U.S. Census, Graham Co., Kansas, shows married, his second and her first, married 17 years.

- [S4985] Cochrane, Family File "Margaret Ann Derr family," 24 Oct 2014, shows year.

- [S12890] Clara Setchell obituary, The Morland Monitor, shows date.

- [S500] Findagrave.com, online, memorial # 143554560, R. Clara Setchell, shows year and includes tombstone photo showing same.

- [S4795] The Gazetteer Co. Inc. Denver Directory, 1951 pg 965, shows her at same address as her daughter Fern; 1953 pg 976, show Fern and her husband, but Clara is not listed.

- [S12890] Clara Setchell obituary, The Morland Monitor, shows date and cemetery.

- [S500] Findagrave.com, online, memorial # 143554560, R. Clara Setchell, includes tombstone photo.

- [S5019] H. J. Setchell household, 1915 Kansas State Census, Graham Co., Kansas, Soloman, shows name as R. Clara Setchell.

- [S5020] Hartley J. Setchell household, 1920 U.S. Census, Graham Co., Kansas, shows name as R. Clara Setchell.

- [S5001] H. F. Shurtz obituary, unknown newspaper, most likely The Beloit Daily Call, shows the family moved when he was 4 years old.

- [S4985] Cochrane, Family File "Margaret Ann Derr family," 24 Oct 2014, shows date, town, county, and state.

- [S500] Findagrave.com, online, memorial # 79601008, Margaret Ann Derr Shurtz, shows date, town, county, and state.

- [S4753] Frederick Shortz household, 1870 U.S. Census, St. Joseph Co., Michigan.

- [S4754] F. Shurtz household, 1880 U.S. Census, Fremont Co., Iowa.

- [S4755] Frederick Shurtz household, 1885 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S5017] Hartley J. Setchell household, 1900 U.S. Census, Phillips Co., Kansas.

- [S5018] H. J. Setchell household, 1910 U.S. Census, Graham Co., Kansas.

- [S5019] H. J. Setchell household, 1915 Kansas State Census, Graham Co., Kansas, Soloman.

- [S5020] Hartley J. Setchell household, 1920 U.S. Census, Graham Co., Kansas.

- [S5021] H. J. Setchell household, 1925 Kansas State Census, Graham Co., Kansas, Soloman Twp.

- [S5021] H. J. Setchell household, 1925 Kansas State Census, Graham Co., Kansas, Soloman Twp., shows him in household.

- [S5022] J. Clara Setchell household, 1930 U.S. Census, Graham Co., Kansas, shows his wife as a widow.

- [S5022] J. Clara Setchell household, 1930 U.S. Census, Graham Co., Kansas.

- [S5022] J. Clara Setchell household, 1930 U.S. Census, Graham Co., Kansas, shows occupation as farmer, industry as general farm.

- [S4795] The Gazetteer Co. Inc. Denver Directory, 1931 pp 2061, 2099.

- [S5023] Roy D. Slagle household, 1940 U.S. Census, Denver City & Co., Colorado.

- [S4795] The Gazetteer Co. Inc. Denver Directory, 1945 pp 1236, 1266; and 1951 pg 965.

- [S12889] Roy D. Slagle household, 1950 U.S. Census, Denver Co., Colorado.

Elenora Shurtz1,2,3

#18972, (1868 - 1922)

Parents

| Father | Frederick J. Shurtz (1832 - 18 May 1892) |

| Mother | Sarah Elizabeth Riegel (20 Mar 1842 - 27 Nov 1920) |

| Ancestry | The Reigel Family |

| Chart Membership | Descendants of Jacob K. and Christiana Ohl Riegel |

| Family Indexes | The Reigel Family |

Key Events:

Burial: Rose Hill Cemetery, Shenandoah, Page Co., Iowa,12

Copyright Notice

The material on this website is subject to copyright.

Facts – names, dates, and places – cannot be copyrighted; you are free to copy them.

But the narratives are my creative work product and are copyrighted. You may copy them for your personal use, but please respect my copyright and do not republish them in any form, including copying them to your tree on Ancestry or elsewhere, unless you have obtained written permission from me.

Many of the images are also copyrighted, and may not be copied without the consent of the copyright holders.

Narrative:

Elenora Shurtz was born on 15 Dec 1868 in MichiganG.4,5,6 She appeared on the 1870 Federal Census of Centerville, St. Joseph Co., MichiganG, in the household of her parents, Frederick J. Shurtz and Sarah Elizabeth Riegel.13

Elenora moved to IowaG Circa 1880 with her parents. She appeared on the 1880 Federal Census of Fisher Twp., Fremont Co., Iowa G, in the household of her parents.14 She appeared on the 1885 State Census of Shenandoah, Page Co., IowaG, in the household of her parents.15 She appeared on the 1895 State Census of Shenandoah, Page Co., IowaG, in the household of her mother.16

Elenora married John H. Eischeid, son of John Eischeid and Margaret Haas, on 20 Oct 1897 in Page Co., IowaG.7,8,9

Elenora and John appeared on the 1900 Federal Census of Shenandoah, Page Co., Iowa G, enumerated 4 Jun 1900, reporting that they owned their home, free of mortgage. Their son Mark was listed as living with them.17

Elenora and John appeared on the 1905 State Census of 312 Valley Ave., Shenandoah, Page Co., IowaG, reporting their home was valued at $1,500. Their son Mark was listed as living with them.18,19,20

Elenora and John appeared on the 1910 Federal Census of Shenandoah, Page Co., Iowa, at 312 Lowell Ave. G, enumerated 12 May 1910, reporting that they owned their home, free of mortgage. Their children Mark and Sarah were listed as living with them.21

Elenora and John appeared on the 1915 State Census of Shenandoah, Page Co., Iowa G, presumably in the same household, although this census does not identify who was living together. He reported that he owned a home valued at $4,000. Their children Mark and Sarah were listed as living with them.22,23,24,25

Elenora and John appeared on the 1920 Federal Census of Shenandoah, Page Co., Iowa, at 512 Elm St. G, enumerated 7 Jan 1920, reporting that they owned their home, free of mortgage. Their children Mark and Sarah were listed as living with them.26

Elenora reported her church affiliation as Congregational.22

Elenora with her husband and daughter, and her brother Harry, drove to Beloit, KansasG, to visit their half brother, Horace, and his family. They made the trip, in a Hudson automobile, in ten hours. According to Google Maps, the trip is now 225 miles and would take four hours.27

Elenora died on 20 Dec 1922 in Grant, Montgomery Co., IowaG, at age 54.10,11 She was buried in Rose Hill Cemetery, Shenandoah, Page Co., IowaG.12

Elenora moved to IowaG Circa 1880 with her parents. She appeared on the 1880 Federal Census of Fisher Twp., Fremont Co., Iowa G, in the household of her parents.14 She appeared on the 1885 State Census of Shenandoah, Page Co., IowaG, in the household of her parents.15 She appeared on the 1895 State Census of Shenandoah, Page Co., IowaG, in the household of her mother.16

Elenora married John H. Eischeid, son of John Eischeid and Margaret Haas, on 20 Oct 1897 in Page Co., IowaG.7,8,9

Elenora and John appeared on the 1900 Federal Census of Shenandoah, Page Co., Iowa G, enumerated 4 Jun 1900, reporting that they owned their home, free of mortgage. Their son Mark was listed as living with them.17

Elenora and John appeared on the 1905 State Census of 312 Valley Ave., Shenandoah, Page Co., IowaG, reporting their home was valued at $1,500. Their son Mark was listed as living with them.18,19,20

Elenora and John appeared on the 1910 Federal Census of Shenandoah, Page Co., Iowa, at 312 Lowell Ave. G, enumerated 12 May 1910, reporting that they owned their home, free of mortgage. Their children Mark and Sarah were listed as living with them.21

Elenora and John appeared on the 1915 State Census of Shenandoah, Page Co., Iowa G, presumably in the same household, although this census does not identify who was living together. He reported that he owned a home valued at $4,000. Their children Mark and Sarah were listed as living with them.22,23,24,25

Elenora and John appeared on the 1920 Federal Census of Shenandoah, Page Co., Iowa, at 512 Elm St. G, enumerated 7 Jan 1920, reporting that they owned their home, free of mortgage. Their children Mark and Sarah were listed as living with them.26

Elenora reported her church affiliation as Congregational.22

Elenora with her husband and daughter, and her brother Harry, drove to Beloit, KansasG, to visit their half brother, Horace, and his family. They made the trip, in a Hudson automobile, in ten hours. According to Google Maps, the trip is now 225 miles and would take four hours.27

Elenora died on 20 Dec 1922 in Grant, Montgomery Co., IowaG, at age 54.10,11 She was buried in Rose Hill Cemetery, Shenandoah, Page Co., IowaG.12

Children:

Children with John H. Eischeid:

- Mark Eischeid (6 Jan 1900 - 3 Jul 1957)

- Sarah Margaret Eischeid+ (1 Jul 1905 - 6 Jun 1976)

Citations

- [S4753] Frederick Shortz household, 1870 U.S. Census, St. Joseph Co., Michigan, shows name as Elnore Shortz.

- [S4754] F. Shurtz household, 1880 U.S. Census, Fremont Co., Iowa, shows name as Ellen N. Shurtz.

- [S500] Findagrave.com, online, memorial # 132184265, Elenora Shurtz Eischeid, and includes tombstone photos showing name as Elenora Eischeid.

- [S500] Findagrave.com, online, memorial # 132184265, Elenora Shurtz Eischeid, shows date and state, and includes tombstone photos showing year. Poster of memorial said in an email that details are from "Rose Hill Cemetery Book 1," published 1995.

- [S4753] Frederick Shortz household, 1870 U.S. Census, St. Joseph Co., Michigan, shows age 1 and state.

- [S4903] John H. Eischied household, 1900 U.S. Census, Page Co., Iowa, shows month, year, age 31, and state.

- [S4746] "County Marriages, 1838-1934," FamilySearch.org, record for John H Eischeid and Elenor Shurtz, citing FHL #1035212, shows date, county, and state.

- [S4903] John H. Eischied household, 1900 U.S. Census, Page Co., Iowa, shows married 2 years.

- [S4904] John H. Eischeid household, 1910 U.S. Census, Page Co., Iowa, shows married 12 years.

- [S5482] "Iowa, County Death Records, 1880-1992," FamilySearch.org, record for Elonora Eischeid, citing FHL # 1535553, shows date, town, county, and state.

- [S500] Findagrave.com, online, memorial # 132184265, Elenora Shurtz Eischeid, shows date, town, as Shenandoah, county, as Page, and state, and includes tombstone photos showing year. Poster of memorial said in an email that details are from "Rose Hill Cemetery Book 1," published 1995.

- [S500] Findagrave.com, online, memorial # 132184265, Elenora Shurtz Eischeid, includes tombstone photos.

- [S4753] Frederick Shortz household, 1870 U.S. Census, St. Joseph Co., Michigan.

- [S4754] F. Shurtz household, 1880 U.S. Census, Fremont Co., Iowa.

- [S4755] Frederick Shurtz household, 1885 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S5072] Sara E. Shurtz household, 1895 Iowa State Census, Page Co., Iowa, Shenandoah ward 1.

- [S4903] John H. Eischied household, 1900 U.S. Census, Page Co., Iowa.

- [S4911] John H. Eischeid card, 1905 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4912] Elnora Eischied card, 1905 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4913] Mark Eischied card, 1905 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4904] John H. Eischeid household, 1910 U.S. Census, Page Co., Iowa.

- [S4907] Mrs. Ella Eischied card, 1915 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4908] J. H. Eischied card, 1915 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4909] Mark Eischied card, 1915 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4910] Sarah M. Eischied card, 1915 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4905] John H. Eischeid household, 1920 U.S. Census, Page Co., Iowa.

- [S4965] "News and Comments," The Beloit Daily Call, 21 Jul 1921.

Harry T. Shurtz1,2,3

#18973, (1871 - 1941)

Parents

| Father | Frederick J. Shurtz (1832 - 18 May 1892) |

| Mother | Sarah Elizabeth Riegel (20 Mar 1842 - 27 Nov 1920) |

| Ancestry | The Reigel Family |

| Chart Membership | Descendants of Jacob K. and Christiana Ohl Riegel |

| Family Indexes | The Reigel Family |

Key Events:

Marriage: 14 Oct 1930, Shenandoah, Page Co., Iowa, Gertrude E. Trusler (b. ca. 1878, d. 28 Nov 1951)7,8

Copyright Notice

The material on this website is subject to copyright.

Facts – names, dates, and places – cannot be copyrighted; you are free to copy them.

But the narratives are my creative work product and are copyrighted. You may copy them for your personal use, but please respect my copyright and do not republish them in any form, including copying them to your tree on Ancestry or elsewhere, unless you have obtained written permission from me.

Many of the images are also copyrighted, and may not be copied without the consent of the copyright holders.

Narrative:

Harry T. Shurtz was born on 22 Oct 1871 in Lockport, MichiganG.4,5,6

Harry moved to IowaG Circa 1880 with his parents. He appeared on the 1880 Federal Census of Fisher Twp., Fremont Co., Iowa, G in the household of his parents, Frederick J. Shurtz and Sarah Elizabeth Riegel.13 He appeared on the 1885 State Census of Shenandoah, Page Co., IowaG, in the household of his parents.14

His given name was Henry at birth, and recorded that way when he was a child. However as an adult he consistently used Harry in all contexts, including legal documents, and that name appears on his tombstone.15,16,17,2,3

The local newspaper in Albany, Gentry Co., MissouriG, reported on 12 Jan 1894 that the Shurtz brothers had arrived from Shenandoah to open a bakery. Which brothers were included is not stated, but we know Harry was there because on 1 May it was reported that he stepped on a board with a nail that penetrated nearly thorough his foot, and on 8 June Charles was reported to be living there, as the senior member of the firm of Shurtz Bros. Harry seems to have returned home soon afterwards as he was back in Shenandoah by 1895.18,19,20

He appeared on the 1895 State Census of Shenandoah, Page Co., IowaG, in the household of his mother.21 He appeared on the 1900 Federal Census of Shenandoah, Page Co., Iowa G, in the household of his mother.22

Harry was working at a bakery in 1895, and operating a cafe and bakery in ShenandoahG by 1900. His younger brothers Wilmer and Charles were also bakers in ShenandoahG, and John was working in a restaurant there, all presumably working in their older brother's shop. After they moved out of town Harry continued to own the cafe and bakery for many years.23,24,25,26,27,28,29

He appeared on the 1905 State Census of 101 Valley Ave., Shenandoah, Page Co., IowaG, in the household of his mother, at 101 Valley Ave.30,31,32 He appeared on the 1910 Federal Census of Shenandoah, Page Co., Iowa G, in the household of his mother.33

He appeared on the 1915 State Census of Shenandoah, Page Co., IowaG. This census does not identify households, but it appears that he was living with his mother since they appear on sequentially numbered cards.34,35 He appeared on the 1920 Federal Census of Shenandoah, Page Co., Iowa G, in the household of his mother.36

Harry and his sister Elenora, with her husband and daughter, drove to Beloit, KansasG, to visit their half brother, Horace, and his family. They made the trip, in a Hudson automobile, in ten hours. According to Google Maps, the trip is now 225 miles and would take four hours.37

Harry T. Shurtz appeared on the 1925 State Census of 706 7th Ave., Shenandoah, Page Co., IowaG, in the household of John H. Eischeid, widower of his late sister, with their two children Mark and Sarah.38 Harry appeared on the 1930 Federal Census of Shenandoah, Page Co., Iowa G, in the household of his late sister Elenora's husband and their two children.39

Harry married Gertrude E. Trusler, daughter of John Trusler and Mary E. Farrell, on 14 Oct 1930 in Shenandoah, Page Co., IowaG, with Rev. James Pearson officiating. She was the widow of Alva Floyd White.7,8

Harry served as councilman in ShenandoahG for 16 years, a length of service not repeated by others in his lifetime. He was elected in 1898 and served until 1909, then from 1921 to 1924, and 1933 to 1935.40,41

In addition to the bakery and cafe, his business interests included brick yards.41 He was evidently retired from active business by 1910 as he reported his occupation as "own income." He owned many business properties, and was a director of the Security Trust and Savings Bank.33,42 In the 1915 state census he reported his occupation as a merchant.35,43

By 1920 he was a proprietor of the Shenandoah Hatchery, a poultry hatchery, in partnership with Floyd F. Bloom. His brother Charles apparently worked for him there after he returned to ShenandoahG about 1936. In 1940 Harry reported that he had worked 72 hours the last week of March, and 50 weeks the prior year. He later sold that business to his partner.44,45,46,47,48,49

Harry and Gertrude appeared on the 1940 Federal Census of Shenandoah, Page Co., Iowa, at 511 West Valley G, enumerated 18 Apr 1940, reporting that they owned a home valued at $2,500, and had lived in the same house in 1935.50

Harry reported his church affiliation as Congregational.38 He died on 15 Sep 1941 at his home at 311 West Valley, Shenandoah, IowaG, at age 69.9,10 He was buried on 17 Sep 1941 in Rose Hill Cemetery, Shenandoah, Page Co., IowaG.11,12

Harry left a will which led to considerable litigation, including two suits that found their way to the Iowa Supreme Court. He left his estate in trust to his nephew, Mark Eischeid, from which his widow, Gertrude, was to received $50 per month for her lifetime from the income, and any additional amount the trustee judged needed for her comfortable support. The remaining net income was to be divided between Mark and his sister Sarah. At the death of the widow they were each to receive one-third of the estate, with the remaining third to be divided between his widow's daughters by her previous marriage, Beatrice and Audry White. However, the widow elected to take instead her widow's one-third share under the law, amounting to about $25,000.51

The income of the trust was reduced by the one-third of the principal taken by the widow, from about $3,300 to about $2,200 annually. But since that election eliminated the monthly payments from income to the widow, Mark and his sister received only an 18½ % reduction in their share. The two step-daughters claimed some of that income should be sequestered so that all parties would receive an equal percentage reduction due to the widow's election. They filed suit to direct the trustee to do so, but the trial court denied their request. The state Supreme Court reversed that finding on 18 Oct 1949, but instead of requiring sequestration of the income directed that an additional amount be paid to the step-daughters when the trust was dissolved.51

A separate case arose around the treatment of certain expenditures by the trustee. The will specified that taxes, assessments, and trustee's expenses were to be paid from the income, thus reducing the amount available to be paid to Mark and his sister. He contended that certain expenditures should be charged to the principal, and thus reduce the amount eventually payable to all beneficiaries, and applied to the probate court for authority to do so. The step-daughters objected, claiming all should be paid from income. The court decided only some should be and both parties appealed. The state Supreme Court decided the case on 6 Mar 1951, making some changes in the lower court ruling. Premiums of the trustee's bond, amounting to $1,406, were to be paid from income. The trustee argued that $142 in taxes on vacant lots should be paid from principal because they produced no income, but the court found that the language of the will required them to be paid from income. Likewise the court held that $460 in city assessments for curbs and gutters were to be paid from income. However the $600 cost of new furnaces for two dwellings that were untenatable when received by the trust, $85 for a new water pipe to another, and cost of installing an indoor toilet in another to meet city requirements, were all found to be payable from principal.52

Harry moved to IowaG Circa 1880 with his parents. He appeared on the 1880 Federal Census of Fisher Twp., Fremont Co., Iowa, G in the household of his parents, Frederick J. Shurtz and Sarah Elizabeth Riegel.13 He appeared on the 1885 State Census of Shenandoah, Page Co., IowaG, in the household of his parents.14

His given name was Henry at birth, and recorded that way when he was a child. However as an adult he consistently used Harry in all contexts, including legal documents, and that name appears on his tombstone.15,16,17,2,3

The local newspaper in Albany, Gentry Co., MissouriG, reported on 12 Jan 1894 that the Shurtz brothers had arrived from Shenandoah to open a bakery. Which brothers were included is not stated, but we know Harry was there because on 1 May it was reported that he stepped on a board with a nail that penetrated nearly thorough his foot, and on 8 June Charles was reported to be living there, as the senior member of the firm of Shurtz Bros. Harry seems to have returned home soon afterwards as he was back in Shenandoah by 1895.18,19,20

He appeared on the 1895 State Census of Shenandoah, Page Co., IowaG, in the household of his mother.21 He appeared on the 1900 Federal Census of Shenandoah, Page Co., Iowa G, in the household of his mother.22

An Enterprising Businessman in ShenandoahG --- Text Stolen from ReigelRidge.com !! ---

Harry was working at a bakery in 1895, and operating a cafe and bakery in ShenandoahG by 1900. His younger brothers Wilmer and Charles were also bakers in ShenandoahG, and John was working in a restaurant there, all presumably working in their older brother's shop. After they moved out of town Harry continued to own the cafe and bakery for many years.23,24,25,26,27,28,29

He appeared on the 1905 State Census of 101 Valley Ave., Shenandoah, Page Co., IowaG, in the household of his mother, at 101 Valley Ave.30,31,32 He appeared on the 1910 Federal Census of Shenandoah, Page Co., Iowa G, in the household of his mother.33

He appeared on the 1915 State Census of Shenandoah, Page Co., IowaG. This census does not identify households, but it appears that he was living with his mother since they appear on sequentially numbered cards.34,35 He appeared on the 1920 Federal Census of Shenandoah, Page Co., Iowa G, in the household of his mother.36

Harry and his sister Elenora, with her husband and daughter, drove to Beloit, KansasG, to visit their half brother, Horace, and his family. They made the trip, in a Hudson automobile, in ten hours. According to Google Maps, the trip is now 225 miles and would take four hours.37

Harry T. Shurtz appeared on the 1925 State Census of 706 7th Ave., Shenandoah, Page Co., IowaG, in the household of John H. Eischeid, widower of his late sister, with their two children Mark and Sarah.38 Harry appeared on the 1930 Federal Census of Shenandoah, Page Co., Iowa G, in the household of his late sister Elenora's husband and their two children.39

Harry married Gertrude E. Trusler, daughter of John Trusler and Mary E. Farrell, on 14 Oct 1930 in Shenandoah, Page Co., IowaG, with Rev. James Pearson officiating. She was the widow of Alva Floyd White.7,8

Harry served as councilman in ShenandoahG for 16 years, a length of service not repeated by others in his lifetime. He was elected in 1898 and served until 1909, then from 1921 to 1924, and 1933 to 1935.40,41

In addition to the bakery and cafe, his business interests included brick yards.41 He was evidently retired from active business by 1910 as he reported his occupation as "own income." He owned many business properties, and was a director of the Security Trust and Savings Bank.33,42 In the 1915 state census he reported his occupation as a merchant.35,43

By 1920 he was a proprietor of the Shenandoah Hatchery, a poultry hatchery, in partnership with Floyd F. Bloom. His brother Charles apparently worked for him there after he returned to ShenandoahG about 1936. In 1940 Harry reported that he had worked 72 hours the last week of March, and 50 weeks the prior year. He later sold that business to his partner.44,45,46,47,48,49

Harry and Gertrude appeared on the 1940 Federal Census of Shenandoah, Page Co., Iowa, at 511 West Valley G, enumerated 18 Apr 1940, reporting that they owned a home valued at $2,500, and had lived in the same house in 1935.50

Harry reported his church affiliation as Congregational.38 He died on 15 Sep 1941 at his home at 311 West Valley, Shenandoah, IowaG, at age 69.9,10 He was buried on 17 Sep 1941 in Rose Hill Cemetery, Shenandoah, Page Co., IowaG.11,12

A Troublesome Will --- Text Stolen from ReigelRidge.com !! ---

Harry left a will which led to considerable litigation, including two suits that found their way to the Iowa Supreme Court. He left his estate in trust to his nephew, Mark Eischeid, from which his widow, Gertrude, was to received $50 per month for her lifetime from the income, and any additional amount the trustee judged needed for her comfortable support. The remaining net income was to be divided between Mark and his sister Sarah. At the death of the widow they were each to receive one-third of the estate, with the remaining third to be divided between his widow's daughters by her previous marriage, Beatrice and Audry White. However, the widow elected to take instead her widow's one-third share under the law, amounting to about $25,000.51

The income of the trust was reduced by the one-third of the principal taken by the widow, from about $3,300 to about $2,200 annually. But since that election eliminated the monthly payments from income to the widow, Mark and his sister received only an 18½ % reduction in their share. The two step-daughters claimed some of that income should be sequestered so that all parties would receive an equal percentage reduction due to the widow's election. They filed suit to direct the trustee to do so, but the trial court denied their request. The state Supreme Court reversed that finding on 18 Oct 1949, but instead of requiring sequestration of the income directed that an additional amount be paid to the step-daughters when the trust was dissolved.51

A separate case arose around the treatment of certain expenditures by the trustee. The will specified that taxes, assessments, and trustee's expenses were to be paid from the income, thus reducing the amount available to be paid to Mark and his sister. He contended that certain expenditures should be charged to the principal, and thus reduce the amount eventually payable to all beneficiaries, and applied to the probate court for authority to do so. The step-daughters objected, claiming all should be paid from income. The court decided only some should be and both parties appealed. The state Supreme Court decided the case on 6 Mar 1951, making some changes in the lower court ruling. Premiums of the trustee's bond, amounting to $1,406, were to be paid from income. The trustee argued that $142 in taxes on vacant lots should be paid from principal because they produced no income, but the court found that the language of the will required them to be paid from income. Likewise the court held that $460 in city assessments for curbs and gutters were to be paid from income. However the $600 cost of new furnaces for two dwellings that were untenatable when received by the trust, $85 for a new water pipe to another, and cost of installing an indoor toilet in another to meet city requirements, were all found to be payable from principal.52

Children:

There were no children with Gertrude E. Trusler

Citations

- [S4759] Sara E. Shurtz household, 1900 U.S. Census, Page Co., Iowa, shows name as Harry T. Shurtz.

- [S4765] Harry T. Shurtz and Gertie E. White, return of marriage to clerk of district court.

- [S500] Findagrave.com, online, memorial # 64871668, Harry T. Shurtz, and includes tombstone photo showing name as H. T. Shurtz.

- [S4756] Henry T. Shurtz, Return of Births in County of St. Joseph, shows date, town, as Lockport, and state.

- [S4754] F. Shurtz household, 1880 U.S. Census, Fremont Co., Iowa, shows age 9 and state.

- [S4765] Harry T. Shurtz and Gertie E. White, return of marriage to clerk of district court, shows age 60 at marriage 14 Oct 1930, town, as Three Rivers, and state.

- [S4765] Harry T. Shurtz and Gertie E. White, return of marriage to clerk of district court, shows date, town, state, officant, his first marriage and her second.

- [S4890] Harry T. Shurtz household, 1940 U.S. Census, Page Co., Iowa, shows married.

- [S6022] "Harry T. Shurtz Dies," Shenandoah Sentinel, 15 Sep 1941, shows died "today," at his home, address.

- [S500] Findagrave.com, online, memorial # 64871668, Harry T. Shurtz, shows date as 18th, and includes tombstone photo showing year.

- [S500] Findagrave.com, online, memorial # 64871668, Harry T. Shurtz, includes tombstone photo.

- [S4783] "Funeral Held in Shenandoah for Mrs. W R Bening's Father," Clarinda Herald-Journal, 18 Sep 1941, shows services were held Wednesday.

- [S4754] F. Shurtz household, 1880 U.S. Census, Fremont Co., Iowa.

- [S4755] Frederick Shurtz household, 1885 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4756] Henry T. Shurtz, Return of Births in County of St. Joseph.

- [S4754] F. Shurtz household, 1880 U.S. Census, Fremont Co., Iowa, shows name as Henry T. Shurtz.

- [S4755] Frederick Shurtz household, 1885 Iowa State Census, Page Co., Iowa, Shenandoah, shows name as Henry F. Shurtz.

- [S4859] Local news, Albany Weekly Ledger, 12 Jan 1894.

- [S4860] Local news, Albany Weekly Ledger, 18 May 1894.

- [S4861] Local news, Albany Weekly Ledger, 8 Jun 1894.

- [S5072] Sara E. Shurtz household, 1895 Iowa State Census, Page Co., Iowa, Shenandoah ward 1.

- [S4759] Sara E. Shurtz household, 1900 U.S. Census, Page Co., Iowa.

- [S5072] Sara E. Shurtz household, 1895 Iowa State Census, Page Co., Iowa, Shenandoah ward 1, shows occupation as __kery, with the beginning cut off in the tight binding.

- [S4759] Sara E. Shurtz household, 1900 U.S. Census, Page Co., Iowa, shows Harry's occupation as bakery & restaurant, and Charles' as baker.

- [S4760] Wilmer A. Shurtz household, 1900 U.S. Census, Page Co., Iowa, shows his occupation as baker.

- [S4915] John Shurtz card, 1905 Iowa State Census, Page Co., Iowa, Shenandoah, shows occupation as work in restaurant.

- [S4914] Harry Shurtz card, 1905 Iowa State Census, Page Co., Iowa, Shenandoah, shows occupation as restaurant & bakery.

- [S6018] "Death of Wilmer Shurtz," Shenandoah World, 4 Sep 1906, shows he was in business with Harry, learning the baking trade from him.

- [S4783] "Funeral Held in Shenandoah for Mrs. W R Bening's Father," Clarinda Herald-Journal, 18 Sep 1941, shows he was a cafe owner and a baker.

- [S4916] Mrs. S. E. Shurtz card, 1905 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4914] Harry Shurtz card, 1905 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4915] John Shurtz card, 1905 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4761] Sarah E. Shurtz household, 1910 U.S. Census, Page Co., Iowa.

- [S4762] Mrs. S. E. Shurtz card, 1915 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4763] Harry Shurtz card, 1915 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4764] Sarah Shurtz household, 1920 U.S. Census, Page Co., Iowa.

- [S4965] "News and Comments," The Beloit Daily Call, 21 Jul 1921.

- [S4906] John H. Eischeid household, 1925 Iowa State Census, Page Co., Iowa, Shenandoah ward 2.

- [S4889] John J. Eischeid household, 1930 U.S. Census, Page Co., Iowa.

- [S4783] "Funeral Held in Shenandoah for Mrs. W R Bening's Father," Clarinda Herald-Journal, 18 Sep 1941.

- [S6022] "Harry T. Shurtz Dies," Shenandoah Sentinel, 15 Sep 1941.

- [S4783] "Funeral Held in Shenandoah for Mrs. W R Bening's Father," Clarinda Herald-Journal, 18 Sep 1941, shows he owned many business properties, and a director.

- [S4765] Harry T. Shurtz and Gertie E. White, return of marriage to clerk of district court, shows occupation as merchant.

- [S4764] Sarah Shurtz household, 1920 U.S. Census, Page Co., Iowa, shows occupation as poultry man, industry as raising poultry2.

- [S4960] Polk's Shenandoah (Iowa) City Directory, 1930, pg 125, shows name of firm and partners.

- [S4889] John J. Eischeid household, 1930 U.S. Census, Page Co., Iowa, shows occupation as owner, industry as hatchery.

- [S4890] Harry T. Shurtz household, 1940 U.S. Census, Page Co., Iowa, shows occupation as proprietor, industry as Shenandoah Hatchery.

- [S4855] Charles Weller Shurtz, Certificate of Death, shows occupation as laborer, industry as chicken hatchery.

- [S6022] "Harry T. Shurtz Dies," Shenandoah Sentinel, 15 Sep 1941, shows he sold the hatchery to his partner.

- [S4890] Harry T. Shurtz household, 1940 U.S. Census, Page Co., Iowa.

- [S4957] Bening et. al. v. Eischeid et. al., 240 Iowa 1295: 300-2.

- [S4958] In re Shurtz's Will, 242 Iowa 450: 560-4.

Charles Weller Shurtz1,2,3

#18974, (1872 - 1938)

Parents

| Father | Frederick J. Shurtz (1832 - 18 May 1892) |

| Mother | Sarah Elizabeth Riegel (20 Mar 1842 - 27 Nov 1920) |

| Ancestry | The Reigel Family |

| Chart Membership | Descendants of Jacob K. and Christiana Ohl Riegel |

| Family Indexes | The Reigel Family |

Key Events:

Marriage: 3 Jun 1894, Albany, Gentry Co., Missouri, Ella May Grubb (b. 24 Apr 1874, d. 14 Jan 1898)8,9,10

Marriage: 30 Mar 1901, York, York Co., Nebraska, Emma Grace Kaufman (b. 4 Apr 1879, d. 3 Feb 1960)11,12

Copyright Notice

The material on this website is subject to copyright.

Facts – names, dates, and places – cannot be copyrighted; you are free to copy them.

But the narratives are my creative work product and are copyrighted. You may copy them for your personal use, but please respect my copyright and do not republish them in any form, including copying them to your tree on Ancestry or elsewhere, unless you have obtained written permission from me.

Many of the images are also copyrighted, and may not be copied without the consent of the copyright holders.

Narrative:

Charles Weller Shurtz was born on 18 Aug 1872 in Lockport, MichiganG.4,5,6,7

Charles moved to IowaG Circa 1880 with his parents. He appeared on the 1880 Federal Census of Fisher Twp., Fremont Co., Iowa, G in the household of his parents, Frederick J. Shurtz and Sarah Elizabeth Riegel.17 He appeared on the 1885 State Census of Shenandoah, Page Co., IowaG, in the household of his parents.18

The local newspaper in Albany, Gentry Co., MissouriG, reported on 12 Jan 1894 that the Shurtz brothers had arrived from Shenandoah to open a bakery. Which brothers were included is not stated, but we know Harry was there because on 1 May it was reported that he stepped on a board with a nail that penetrated nearly thorough his foot, and on 8 June Charles was reported to be living there, as the senior member of the firm of Shurtz Bros. Harry seems to have returned home soon afterwards as he was back in Shenandoah by 1895.19,20,21

Apparently they, or at least Charles, did open a local business, as an ad in Dec 1895 announced "All kinds of fruits and candies at Shurtz's." And in 1899 Charles was called the former proprietor of the City Bakery and Restaurant.22,23

Charles married first Ella May Grubb, daughter of Allen W. Grubb and Margaret Ann Murphy, on 3 Jun 1894 in Albany, Gentry Co., MissouriG, at the residence of the bride's parents, with Rev. William W. Burks officiating.8,9,10

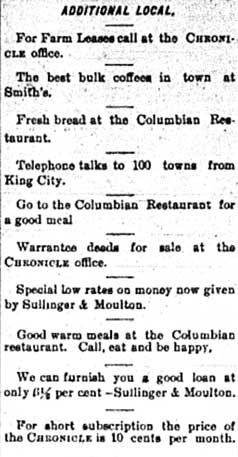

Charles and Ella moved 25 miles away to King CityG in Jun 1897, when Charles purchased the Columbian Restaurant there.24,25 Charles immediately began running a series of "local ads" in the weekly newspaper in that town. Local ads were typically two-line simple text statements, intermixed in a column with short news items about local people or events. He ran these ads weekly until the death of his wife in Jan 1898, then intermittently after that.27

Charles immediately began running a series of "local ads" in the weekly newspaper in that town. Local ads were typically two-line simple text statements, intermixed in a column with short news items about local people or events. He ran these ads weekly until the death of his wife in Jan 1898, then intermittently after that.27

His wife died on 14 Jan 1898 in Albany, Gentry Co., MissouriG.28,29 On 6 May 1898 the local newspaper reported that Charles had sold the Columbian Restaurant to Joe Frederick "this week."30

There is a perplexing report in the local paper on 1 Apr 1898. It says "Mrs. Imel of St. Joe is a guest of her sister, Mrs. Shurtz." The only known Mrs. Shurtz in town had died three months before, so it seems the reference should have been to Charles. "Mrs. Imel" could refer to Charles' aunt Violetta who was living in St. Joseph at that time, or to her sister-in-law or either of two daughters-in-law who also lived in that city then. But it seems most likely that the news item was largely confused, and it was Violetta visiting her bereaved nephew.31

Charles, spent some months in Mt. Ayr, IowaG, then stopped by Albany in Feb 1899 to visit friends on his way back to Shenandoah.32 He appeared on the 1900 Federal Census of Shenandoah, Page Co., Iowa G, in the household of his mother.33

Charles evidently maintained close ties to his late wife's family after her death, as he returned to AlbanyG in Oct 1899 to visit the family when his former father-in-law was terminally ill.23

Charles married second Emma Grace Kaufman, daughter of Philip Kaufman and Rachel Melvina Fagin, on 30 Mar 1901 in York, York Co., NebraskaG, with Rev. George J. Chapman officiating.11,12

Charles's older brother Harry was working at a bakery in 1895, and operating a cafe and bakery in ShenandoahG by 1900. Charles and his brother Wilmer were also bakers there in their older brother's shop.34,35,36,37,38,39,40

Charles and Grace moved to Nelson, Nuckolls Co., NebraskaG, Before 1910. He and his brother John were operating a restaurant/bakery there by 1910.41 Charles and Grace appeared on the 1910 Federal Census of Nelson, Nuckolls Co., Nebraska G, enumerated 25 Apr 1910, reporting they rented their home. His younger brother John was listed as living with them.42

Charles and Grace moved to Omaha by 1912, when they were living at 1106 South 10th St. They changed their residence frequently over the next six years, in most cases being listed as rooming or boarding. Addresses included 1013 South 11th St. in 1913, 1421 24th St. and 318½ South 20th St. in 1915, 2019 Harney St. in 1916 and 1917, and the Elms Hotel in 1918.43

After coming to Omaha Charles worked as a baker for a number of years for William D. Vodric, who owned a bakery at 213 South 20th St. He worked there until about 1918.44 By 1920 Charles opened his own bakery at 2301 Leavenworth St., in partnership William Gemmer. That business lasted until at least 1923.45,46

Charles and Grace appeared on the 1920 Federal Census of Omaha, Douglas Co., Nebraska, at 408 South 24th St. G, enumerated 9 Jan 1920, rooming at the home of Elwood Moore and his family with six other roomers.47 Circa 1921 they moved to 2324 Harney St.G, then by 1925 to 412 South 24th St., to 1721 Davenport about 1926, then to 1811 Chicago by 1928.48

After his bakery closed Charles worked for a time at the restaurant owned by George H. Hansen, a block up the street at 2402 Leavenworth St.49 Circa 1926 Charles opened his own bakery again, calling it the Carter Lake Bakery, at 1518 Locust St.G.50,51

Circa 1929 Charles and Grace moved to 216 North 17th St., and were variously reported in 214, 216, and 218 for the remainder of their time in Omaha. It is not clear whether they actually moved between the nearby houses or whether these were errors in the city directory.52 Charles and Grace appeared on the 1930 Federal Census of Omaha, Douglas Co., Nebraska G, at 214 North 17th St., enumerated 10 Apr 1930, reporting that they were renting their home, apparently half of a two-family house, for $28 per month.53

He operated his bakery until about 1933, when it came under the ownership of John B. Gurler. After that he worked as a laborer until he and his wife left OmahaG.54

Charles and Grace moved back to his home town of Shenandoah, IowaG, Circa 1936, where they lived until his death.55 Charles worked there as a laborer in a chicken hatchery, apparently the one operated by his brother Harry.56,57,58,59,60,61

Charles died on 3 May 1938 in Shenandoah, Page Co., IowaG, at age 65.13,14 He was buried on 5 May 1938 in Rose Hill Cemetery, Shenandoah, Page Co., IowaG.15,16

Charles moved to IowaG Circa 1880 with his parents. He appeared on the 1880 Federal Census of Fisher Twp., Fremont Co., Iowa, G in the household of his parents, Frederick J. Shurtz and Sarah Elizabeth Riegel.17 He appeared on the 1885 State Census of Shenandoah, Page Co., IowaG, in the household of his parents.18

Opening a Bakery in Albany, MissouriG, --- Text Stolen from ReigelRidge.com !! ---

The local newspaper in Albany, Gentry Co., MissouriG, reported on 12 Jan 1894 that the Shurtz brothers had arrived from Shenandoah to open a bakery. Which brothers were included is not stated, but we know Harry was there because on 1 May it was reported that he stepped on a board with a nail that penetrated nearly thorough his foot, and on 8 June Charles was reported to be living there, as the senior member of the firm of Shurtz Bros. Harry seems to have returned home soon afterwards as he was back in Shenandoah by 1895.19,20,21

Apparently they, or at least Charles, did open a local business, as an ad in Dec 1895 announced "All kinds of fruits and candies at Shurtz's." And in 1899 Charles was called the former proprietor of the City Bakery and Restaurant.22,23

Charles married first Ella May Grubb, daughter of Allen W. Grubb and Margaret Ann Murphy, on 3 Jun 1894 in Albany, Gentry Co., MissouriG, at the residence of the bride's parents, with Rev. William W. Burks officiating.8,9,10

Charles and Ella moved 25 miles away to King CityG in Jun 1897, when Charles purchased the Columbian Restaurant there.24,25

"Local ads" including three from Charles' Columbian Restaurant

from King City Chronicle 25 Apr 189826

from King City Chronicle 25 Apr 189826

His wife died on 14 Jan 1898 in Albany, Gentry Co., MissouriG.28,29 On 6 May 1898 the local newspaper reported that Charles had sold the Columbian Restaurant to Joe Frederick "this week."30

There is a perplexing report in the local paper on 1 Apr 1898. It says "Mrs. Imel of St. Joe is a guest of her sister, Mrs. Shurtz." The only known Mrs. Shurtz in town had died three months before, so it seems the reference should have been to Charles. "Mrs. Imel" could refer to Charles' aunt Violetta who was living in St. Joseph at that time, or to her sister-in-law or either of two daughters-in-law who also lived in that city then. But it seems most likely that the news item was largely confused, and it was Violetta visiting her bereaved nephew.31

Charles, spent some months in Mt. Ayr, IowaG, then stopped by Albany in Feb 1899 to visit friends on his way back to Shenandoah.32 He appeared on the 1900 Federal Census of Shenandoah, Page Co., Iowa G, in the household of his mother.33

Charles evidently maintained close ties to his late wife's family after her death, as he returned to AlbanyG in Oct 1899 to visit the family when his former father-in-law was terminally ill.23

Charles married second Emma Grace Kaufman, daughter of Philip Kaufman and Rachel Melvina Fagin, on 30 Mar 1901 in York, York Co., NebraskaG, with Rev. George J. Chapman officiating.11,12

Charles's older brother Harry was working at a bakery in 1895, and operating a cafe and bakery in ShenandoahG by 1900. Charles and his brother Wilmer were also bakers there in their older brother's shop.34,35,36,37,38,39,40

Moving to NebraskaG --- Text Stolen from ReigelRidge.com !! ---

Charles and Grace moved to Nelson, Nuckolls Co., NebraskaG, Before 1910. He and his brother John were operating a restaurant/bakery there by 1910.41 Charles and Grace appeared on the 1910 Federal Census of Nelson, Nuckolls Co., Nebraska G, enumerated 25 Apr 1910, reporting they rented their home. His younger brother John was listed as living with them.42

Charles and Grace moved to Omaha by 1912, when they were living at 1106 South 10th St. They changed their residence frequently over the next six years, in most cases being listed as rooming or boarding. Addresses included 1013 South 11th St. in 1913, 1421 24th St. and 318½ South 20th St. in 1915, 2019 Harney St. in 1916 and 1917, and the Elms Hotel in 1918.43

After coming to Omaha Charles worked as a baker for a number of years for William D. Vodric, who owned a bakery at 213 South 20th St. He worked there until about 1918.44 By 1920 Charles opened his own bakery at 2301 Leavenworth St., in partnership William Gemmer. That business lasted until at least 1923.45,46

Charles and Grace appeared on the 1920 Federal Census of Omaha, Douglas Co., Nebraska, at 408 South 24th St. G, enumerated 9 Jan 1920, rooming at the home of Elwood Moore and his family with six other roomers.47 Circa 1921 they moved to 2324 Harney St.G, then by 1925 to 412 South 24th St., to 1721 Davenport about 1926, then to 1811 Chicago by 1928.48

After his bakery closed Charles worked for a time at the restaurant owned by George H. Hansen, a block up the street at 2402 Leavenworth St.49 Circa 1926 Charles opened his own bakery again, calling it the Carter Lake Bakery, at 1518 Locust St.G.50,51

Circa 1929 Charles and Grace moved to 216 North 17th St., and were variously reported in 214, 216, and 218 for the remainder of their time in Omaha. It is not clear whether they actually moved between the nearby houses or whether these were errors in the city directory.52 Charles and Grace appeared on the 1930 Federal Census of Omaha, Douglas Co., Nebraska G, at 214 North 17th St., enumerated 10 Apr 1930, reporting that they were renting their home, apparently half of a two-family house, for $28 per month.53

Losing His Bakery --- Text Stolen from ReigelRidge.com !! ---

He operated his bakery until about 1933, when it came under the ownership of John B. Gurler. After that he worked as a laborer until he and his wife left OmahaG.54

Charles and Grace moved back to his home town of Shenandoah, IowaG, Circa 1936, where they lived until his death.55 Charles worked there as a laborer in a chicken hatchery, apparently the one operated by his brother Harry.56,57,58,59,60,61

Charles died on 3 May 1938 in Shenandoah, Page Co., IowaG, at age 65.13,14 He was buried on 5 May 1938 in Rose Hill Cemetery, Shenandoah, Page Co., IowaG.15,16

Children:

Children with Ella May Grubb:

- Frederick A. Shurtz (ca. 1896 - ca. 1896)

- Elmer M. Shurtz (14 Jan 1898 - 18 Jan 1898)

Children:

There were no children with Emma Grace Kaufman

Citations

- [S4855] Charles Weller Shurtz, Certificate of Death.

- [S4758] Charles Shurtz, Return of Births in County of St. Joseph.

- [S4754] F. Shurtz household, 1880 U.S. Census, Fremont Co., Iowa, shows name as Charles W. Shurtz.

- [S4758] Charles Shurtz, Return of Births in County of St. Joseph, shows date, town, and state.

- [S4855] Charles Weller Shurtz, Certificate of Death, shows date, town, as Three Rivers, and state.

- [S4754] F. Shurtz household, 1880 U.S. Census, Fremont Co., Iowa, shows age 7 and state.

- [S4851] Charles W. Schultz household, 1910 U.S. Census, Nuckolls Co., Nebraska, shows age 37 and state.

- [S4857] Charles W. Shurtz and Ella M. Grubb, Marriage License, shows date, town, county, state, and officiant.

- [S4861] Local news, Albany Weekly Ledger, 8 Jun 1894, shows date, town, and at her parents' home.

- [S4871] Ella M. Shurtz grave marker, shows her as his wife.

- [S4864] Charles W. Shurtz and Emma G. Kaufman, Marriage Record, shows date, town, county, state, and officant.

- [S4851] Charles W. Schultz household, 1910 U.S. Census, Nuckolls Co., Nebraska, shows married 9 years, his second marriage an her first.

- [S4855] Charles Weller Shurtz, Certificate of Death, shows date, town, county, and state.

- [S500] Findagrave.com, online, memorial # 64866088, Charles W. Shurtz, shows date and includes tombstone photos showing year.

- [S4855] Charles Weller Shurtz, Certificate of Death, shows date, town, state.

- [S500] Findagrave.com, online, memorial # 64866088, Charles W. Shurtz, includes tombstone photos.

- [S4754] F. Shurtz household, 1880 U.S. Census, Fremont Co., Iowa.

- [S4755] Frederick Shurtz household, 1885 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4859] Local news, Albany Weekly Ledger, 12 Jan 1894.

- [S4860] Local news, Albany Weekly Ledger, 18 May 1894.

- [S4861] Local news, Albany Weekly Ledger, 8 Jun 1894.

- [S4884] Local news, Albany Weekly Ledger, 27 Dec 1895, same ad ran the week before.

- [S4883] "Home News," Albany Weekly Ledger, 6 Oct 1899.

- [S5101] "Personal Mention," The King City Chronicle, 18 Jun 1897, shows him as new proprietor.

- [S4862] "Obituary," Albany Weekly Ledger, 21 Jan 1898, shows she was from King City.

- [S5002] "H. F. Shurtz & Sons," The Beloit Daily Call, 24 Jun 1919.

- [S5102] "Additional Local," The King City Chronicle, 25 Apr 1898.

- [S4967] "Obituary," The King City Chronicle, 21 Jan 1898, shows date, city, and at father's home.

- [S4871] Ella M. Shurtz grave marker, shows date.

- [S5105] "Local Gatherings," The King City Chronicle, 6 May 1898.

- [S5106] "Local Gatherings," The King City Chronicle, 1 Apr 1898.

- [S4901] "Home News," Albany Weekly Ledger, 10 Feb 1899.

- [S4759] Sara E. Shurtz household, 1900 U.S. Census, Page Co., Iowa.

- [S5072] Sara E. Shurtz household, 1895 Iowa State Census, Page Co., Iowa, Shenandoah ward 1, shows occupation as __kery, with the beginning cut off in the tight binding.

- [S4759] Sara E. Shurtz household, 1900 U.S. Census, Page Co., Iowa, shows Harry's occupation as bakery & restaurant, and Charles' as baker.

- [S4760] Wilmer A. Shurtz household, 1900 U.S. Census, Page Co., Iowa, shows his occupation as baker.

- [S4915] John Shurtz card, 1905 Iowa State Census, Page Co., Iowa, Shenandoah, shows occupation as work in restaurant.

- [S4914] Harry Shurtz card, 1905 Iowa State Census, Page Co., Iowa, Shenandoah, shows occupation as restaurant & bakery.

- [S6018] "Death of Wilmer Shurtz," Shenandoah World, 4 Sep 1906, shows he was in business with Harry, learning the baking trade from him.

- [S4783] "Funeral Held in Shenandoah for Mrs. W R Bening's Father," Clarinda Herald-Journal, 18 Sep 1941, shows he was a cafe owner and a baker.

- [S4851] Charles W. Schultz household, 1910 U.S. Census, Nuckolls Co., Nebraska, shows Charles' occupation as baker, with "partner" written above, and industry as restaurant, and John's occupation as restaurant and something obscured, and industry as restaurant with "partner" written above.

- [S4851] Charles W. Schultz household, 1910 U.S. Census, Nuckolls Co., Nebraska.

- [S4853] Omaha Directory Co.'s Omaha City Directory, 1912 pg 801; 1913 pg 832; 1914 pg 816; 1915 pg 798; 1916 pg 898; 1917 pg 742; and 1918 pg 819.

- [S4853] Omaha Directory Co.'s Omaha City Directory, 1912 pg 801; 1913 pg 832; 1914 pg 816; 1915 pp 798, 892; 1916 pg 898; 1917 pg 742; and 1918 pg 819.

- [S4854] R. L. Polk & Co.'s City Directory of Greater Omaha, 1920 pg 828; 1921 pg 836; and 1923 pg 943.

- [S4848] Elwood Moore household, 1920 U.S. Census, Douglas Co., Nebraska, shows occupation as proprietor, industry as bakery.

- [S4848] Elwood Moore household, 1920 U.S. Census, Douglas Co., Nebraska.

- [S4854] R. L. Polk & Co.'s City Directory of Greater Omaha, 1921 pg 836; 1923 pg 943; 1925 pg 856; 1926 pg 776; and 1928 pg 837.

- [S4854] R. L. Polk & Co.'s City Directory of Greater Omaha, 1925 pp 379, 856.

- [S4854] R. L. Polk & Co.'s City Directory of Greater Omaha, 1926 pp 167, 776; and 1933 pg 690.

- [S4849] Charles Shurtz household, 1930 U.S. Census, Douglas Co., Nebraska, shows occupation as proprietor, industry as bakery.

- [S4854] R. L. Polk & Co.'s City Directory of Greater Omaha, 1929 pg 666; 1931 pg 768; 1932 pg 707; 1933 pg 690; 1934 pg 720; and 1935 pg 773.

- [S4849] Charles Shurtz household, 1930 U.S. Census, Douglas Co., Nebraska.

- [S4854] R. L. Polk & Co.'s City Directory of Greater Omaha, 1934 pp 179, 720; and 1935 pg 773.

- [S4855] Charles Weller Shurtz, Certificate of Death, shows he had lived in town 2 years.

- [S4764] Sarah Shurtz household, 1920 U.S. Census, Page Co., Iowa, shows occupation as poultry man, industry as raising poultry2.

- [S4960] Polk's Shenandoah (Iowa) City Directory, 1930, pg 125, shows name of firm and partners.

- [S4889] John J. Eischeid household, 1930 U.S. Census, Page Co., Iowa, shows occupation as owner, industry as hatchery.

- [S4890] Harry T. Shurtz household, 1940 U.S. Census, Page Co., Iowa, shows occupation as proprietor, industry as Shenandoah Hatchery.

- [S4855] Charles Weller Shurtz, Certificate of Death, shows occupation as laborer, industry as chicken hatchery.

- [S6022] "Harry T. Shurtz Dies," Shenandoah Sentinel, 15 Sep 1941, shows he sold the hatchery to his partner.

Edwin Willard Schurz1,2,3

#18975, (1874 - 1938)

Parents

| Father | Frederick J. Shurtz (1832 - 18 May 1892) |

| Mother | Sarah Elizabeth Riegel (20 Mar 1842 - 27 Nov 1920) |

| Ancestry | The Reigel Family |

| Chart Membership | Descendants of Jacob K. and Christiana Ohl Riegel |

| Family Indexes | The Reigel Family |

Key Events:

Marriage: 17 Jan 1913, La Porte Co., Indiana, Mary Edith Morrison (b. 1 Feb 1880, d. 18 Oct 1913)7,8,9

Marriage: 26 Oct 1921, Grand Rapids, Kent Co., Michigan, Genevieve Newlin (b. 16 Feb 1892, d. 25 Apr 1967)10,11,12

Copyright Notice

The material on this website is subject to copyright.

Facts – names, dates, and places – cannot be copyrighted; you are free to copy them.

But the narratives are my creative work product and are copyrighted. You may copy them for your personal use, but please respect my copyright and do not republish them in any form, including copying them to your tree on Ancestry or elsewhere, unless you have obtained written permission from me.

Many of the images are also copyrighted, and may not be copied without the consent of the copyright holders.

Narrative:

Edwin Willard Schurz was born on 18 Jul 1874 in Lockport, MichiganG.4,5,6

Edwin moved to IowaG Circa 1880 with his parents. He appeared on the 1880 Federal Census of Fisher Twp., Fremont Co., Iowa, G in the household of his parents, Frederick J. Shurtz and Sarah Elizabeth Riegel.17 He appeared on the 1885 State Census of Shenandoah, Page Co., IowaG, in the household of his parents.18

Edwin moved to Chicago, IllinoisG, by 1896.19 A Pennsylvania paper reported in Apr 1896 that he had returned to his parents' home town, MiltonG, to visit friends there.20

Edwin appeared on the 1900 Federal Census of Chicago, Cook Co., Illinois, at 25 46th St. G, enumerated 12 Jun 1900, boarding with Alice Morse and her sister, along with six other men and one woman, all with office jobs, including one lawyer.21

By 1900 Edwin was a stenographer. Sometime between then and 1910 he formed a relationship with Hobart M. Cable, Jr., for whom he worked the rest of his career. Hobart Sr. had been in the piano business with his brothers, and had than founded his own piano manufacturing business, The Hobart M. Cable Co., with a factory in La Porte, IndianaG. By 1910 he had died and Hobart Jr. had succeeded him as president of the company, and Edwin was working there as a clerk.22,23,24

Edwin appeared on the 1910 Federal Census of Chicago, Cook Co., Illinois, at 1438 G, enumerated 18 Apr 1910, lodging with H. M. Cable, his mother, sister, and her son and a Swedish servant. Cable, at 28, was the president of the piano factory where Edwin worked.25

Circa 1910 the company offices were moved to La Porte. Edwin, then an auditor for the firm, moved there as well, boarding at 1627 Michigan Ave.26 He was treasurer of the company by 1913.27,28,29

His birth name was Edwin Willard Shurtz, and he seems to have used that spelling of his surname until he moved to Indiana sometime after 1900. About 1913 he seems to have adopted the spelling Schurz, which he and his family used thereafter.30,31,32,33,34,2,1

Edwin married first Mary Edith Morrison, daughter of Henry D. Morrison and Mary Naomi Ridgeway, on 17 Jan 1913 in La Porte Co., IndianaG.7,8,9

On 18 Oct 1913, nine months after their marriage, Edwin was driving his Pierce-Arrow touring car carrying his wife Edith and three other women when he approached what was called the most dangerous railroad crossing in northern Indiana, four miles north of La PorteG. His view obstructed by a high embankment, he failed to see a freight train, with the engine pushing a box car ahead. The train struck the auto fatally injuring all four women. Edwin was reported as probably fatally injured, but managed to bring his wife to a farm house a half mile away where doctors were summoned, to no avail.35,36

His wife died on 18 Oct 1913 in La Porte, IndianaG.36,37

By 1918 was living at a fine home at 1311 Michigan Ave.G No record has been found indicating when he bought it, though is might be supposed it was with his first wife.

Edwin registered for the draft for World War I on 12 Sep 1918, while living at 1311 Michigan Ave., La Porte, IndianaG, reporting he was employed as an official at Hobart M. Cable Co. in La Porte.1

Edwin appeared on the 1920 Federal Census of La Porte, La Porte Co., Indiana, at 1311 Michigan Ave. G, enumerated 13 Jan 1920, reporting that he owned his home, free of mortgage. Ella Schuny, a 52-year-old housekeeper, was listed as living with him.3

Edwin married second Genevieve Newlin, daughter of Charles M. Newlin and Nancy Odenbaugh, on 26 Oct 1921 in Grand Rapids, Kent Co., MichiganG, at the home of Mr. and Mrs. Lewis Seal Reynolds, with Rev. William Samuel Hess officiating.10,11,12

Circa 1929 The Deluxe Products Corp., a manufacturer of light weight castings, cast iron pistons, and steel oil filters, was formed. Hobart Cable was president and Edwin was secretary, while retaining their positions in the piano company. Edwin's new father-in-law, Charles M. Newlin, was comptroller.38,39 Edwin held both the secretary and treasurer offices in both companies by 1938.40,41

Edwin and Genevieve appeared on the 1930 Federal Census of La Porte, La Porte Co., Indiana, at 1311 Michigan Ave. G, enumerated 19 Apr 1930, reporting that they owned a home valued at $20,000, and owned a radio. Their children Sara and Edwin were listed as living with them, as was Sarah Hostettler, a 30-year-old servant.42

Edwin and Genevieve moved to 1503 Indiana Ave.G by 1938.43

Edwin died on 10 Jul 1938, at his home, 1503 Indiana Ave., La Porte, La Porte Co., IndianaG, at age 63.13,14 He was buried on 12 Jul 1938 in Pine Lake Cemetery, La Porte, IndianaG.15,16

Edwin moved to IowaG Circa 1880 with his parents. He appeared on the 1880 Federal Census of Fisher Twp., Fremont Co., Iowa, G in the household of his parents, Frederick J. Shurtz and Sarah Elizabeth Riegel.17 He appeared on the 1885 State Census of Shenandoah, Page Co., IowaG, in the household of his parents.18

Edwin moved to Chicago, IllinoisG, by 1896.19 A Pennsylvania paper reported in Apr 1896 that he had returned to his parents' home town, MiltonG, to visit friends there.20

Edwin appeared on the 1900 Federal Census of Chicago, Cook Co., Illinois, at 25 46th St. G, enumerated 12 Jun 1900, boarding with Alice Morse and her sister, along with six other men and one woman, all with office jobs, including one lawyer.21

Establishing a Career with Cable Piano Company --- Text Stolen from ReigelRidge.com !! ---

By 1900 Edwin was a stenographer. Sometime between then and 1910 he formed a relationship with Hobart M. Cable, Jr., for whom he worked the rest of his career. Hobart Sr. had been in the piano business with his brothers, and had than founded his own piano manufacturing business, The Hobart M. Cable Co., with a factory in La Porte, IndianaG. By 1910 he had died and Hobart Jr. had succeeded him as president of the company, and Edwin was working there as a clerk.22,23,24

Edwin appeared on the 1910 Federal Census of Chicago, Cook Co., Illinois, at 1438 G, enumerated 18 Apr 1910, lodging with H. M. Cable, his mother, sister, and her son and a Swedish servant. Cable, at 28, was the president of the piano factory where Edwin worked.25

Circa 1910 the company offices were moved to La Porte. Edwin, then an auditor for the firm, moved there as well, boarding at 1627 Michigan Ave.26 He was treasurer of the company by 1913.27,28,29

His birth name was Edwin Willard Shurtz, and he seems to have used that spelling of his surname until he moved to Indiana sometime after 1900. About 1913 he seems to have adopted the spelling Schurz, which he and his family used thereafter.30,31,32,33,34,2,1

Edwin married first Mary Edith Morrison, daughter of Henry D. Morrison and Mary Naomi Ridgeway, on 17 Jan 1913 in La Porte Co., IndianaG.7,8,9

The Tragic End of His First Marriage --- Text Stolen from ReigelRidge.com !! ---

On 18 Oct 1913, nine months after their marriage, Edwin was driving his Pierce-Arrow touring car carrying his wife Edith and three other women when he approached what was called the most dangerous railroad crossing in northern Indiana, four miles north of La PorteG. His view obstructed by a high embankment, he failed to see a freight train, with the engine pushing a box car ahead. The train struck the auto fatally injuring all four women. Edwin was reported as probably fatally injured, but managed to bring his wife to a farm house a half mile away where doctors were summoned, to no avail.35,36

His wife died on 18 Oct 1913 in La Porte, IndianaG.36,37

By 1918 was living at a fine home at 1311 Michigan Ave.G No record has been found indicating when he bought it, though is might be supposed it was with his first wife.

Edwin registered for the draft for World War I on 12 Sep 1918, while living at 1311 Michigan Ave., La Porte, IndianaG, reporting he was employed as an official at Hobart M. Cable Co. in La Porte.1

Edwin appeared on the 1920 Federal Census of La Porte, La Porte Co., Indiana, at 1311 Michigan Ave. G, enumerated 13 Jan 1920, reporting that he owned his home, free of mortgage. Ella Schuny, a 52-year-old housekeeper, was listed as living with him.3

Edwin married second Genevieve Newlin, daughter of Charles M. Newlin and Nancy Odenbaugh, on 26 Oct 1921 in Grand Rapids, Kent Co., MichiganG, at the home of Mr. and Mrs. Lewis Seal Reynolds, with Rev. William Samuel Hess officiating.10,11,12

Starting Deluxe Products Corp. --- Text Stolen from ReigelRidge.com !! ---

Circa 1929 The Deluxe Products Corp., a manufacturer of light weight castings, cast iron pistons, and steel oil filters, was formed. Hobart Cable was president and Edwin was secretary, while retaining their positions in the piano company. Edwin's new father-in-law, Charles M. Newlin, was comptroller.38,39 Edwin held both the secretary and treasurer offices in both companies by 1938.40,41

Edwin and Genevieve appeared on the 1930 Federal Census of La Porte, La Porte Co., Indiana, at 1311 Michigan Ave. G, enumerated 19 Apr 1930, reporting that they owned a home valued at $20,000, and owned a radio. Their children Sara and Edwin were listed as living with them, as was Sarah Hostettler, a 30-year-old servant.42

Edwin and Genevieve moved to 1503 Indiana Ave.G by 1938.43

Edwin died on 10 Jul 1938, at his home, 1503 Indiana Ave., La Porte, La Porte Co., IndianaG, at age 63.13,14 He was buried on 12 Jul 1938 in Pine Lake Cemetery, La Porte, IndianaG.15,16

Children:

There were no children with Mary Edith Morrison

Children:

Children with Genevieve Newlin:

- Sara Schurz (ca. 1923 - 21 Nov 2015)

- Edwin Williard Schurz (27 Dec 1924 - 10 Jul 2010)

Citations

- [S4812] Edwin Williard Schurz, World War I Selective Service System Draft Registration Cards, 1917-1918.

- [S3682] "Iowa, Marriages, 1780-1992," FamilySearch.org, record for Edwin Williard Schurz and Mary Edith Morrison, citing FHL #1673874.

- [S4840] Edward W. Schurz household, 1920 U.S. Census, La Porte Co., Indiana.

- [S4757] Edwin N. Shurtz, Return of Births in County of St. Joseph, shows date, town, as Lockport, and state.

- [S4812] Edwin Williard Schurz, World War I Selective Service System Draft Registration Cards, 1917-1918, shows date.

- [S2785] Marriage Register, State Copy, Michigan, 1921, Kent Co., no. 14168, Edwin W. Schurz and Genevive Newlin, shows age 47 at marriage 26 Oct 1921, town, as Three Rivers, and state.

- [S3682] "Iowa, Marriages, 1780-1992," FamilySearch.org, record for Edwin Williard Schurz and Mary Edith Morrison, citing FHL #1673874, shows date; film is for La Porte Co.

- [S4814] "4 Die in Auto Crash," The Washington Post, 19 Oct 1913, shows they were married about a year before.

- [S4840] Edward W. Schurz household, 1920 U.S. Census, La Porte Co., Indiana, shows him as a widower.

- [S2785] Marriage Register, State Copy, Michigan, 1921, Kent Co., no. 14168, Edwin W. Schurz and Genevive Newlin, shows date, city, county, state, officant, as W. S. Hess, and his second and her first marriage.

- [S6021] Clipping reprinted from Grand Rapids Press, Grand Rapids, Michigan dated 27 Oct 1921, Tri-Weekly Sentinel Post, 28 Nov 1921, shows wedding was Wednesday, location, and officiant.

- [S4810] Edwin Schurz household, 1930 U.S. Census, La Porte Co., Indiana, shows married, with his first marriage at age 39, and hers at 29.

- [S12882] Edwen Williard Schurz, Certificate of Death, shows date, address, city, county, and state.

- [S4831] Cemetery & Research Association of La Porte County, Indiana, online, "Pine Lake Random Photos Q to T Taken December of 2011," entry for Edwin W. Schurz, shows year and includes tombstone photo showing same.

- [S12882] Edwen Williard Schurz, Certificate of Death, shows date and cemetery.

- [S4831] Cemetery & Research Association of La Porte County, Indiana, online, "Pine Lake Random Photos Q to T Taken December of 2011," entry for Edwin W. Schurz, includes tombstone photo.

- [S4754] F. Shurtz household, 1880 U.S. Census, Fremont Co., Iowa.

- [S4755] Frederick Shurtz household, 1885 Iowa State Census, Page Co., Iowa, Shenandoah.

- [S4841] "Milton Melange," Philadelphia Inquirer, 26 Apr 1896, shows he was visiting from Chicago.

- [S4841] "Milton Melange," Philadelphia Inquirer, 26 Apr 1896.

- [S4839] Alice L. Morse household, 1900 U.S. Census, Cook Co., Illinois.

- [S4839] Alice L. Morse household, 1900 U.S. Census, Cook Co., Illinois, shows occupation as stenographer.

- [S4838] H M Cable household, 1910 U.S. Census, Cook Co., Illinois, shows Cable as president and Edwin as clerk, industry as piano factory.

- [S4844] LaPorte Directory, 1904 pg 41, shows The Hobart M. Cable Co. at Bosserman and Factory.

- [S4838] H M Cable household, 1910 U.S. Census, Cook Co., Illinois.

- [S4842] Bumstead's La Porte City and Business Directory, 1910-1911 pg 80, shows Hobart Jr. as president and living on Michigan Ave.; pg 234, shows Edwin as auditor and address.

- [S4843] Smith's Directory of La Porte, Ind., 1913 pp 57, 234.

- [S4814] "4 Die in Auto Crash," The Washington Post, 19 Oct 1913, shows he was treasurer of a piano company.

- [S4840] Edward W. Schurz household, 1920 U.S. Census, La Porte Co., Indiana, shows occupation as treasurer, industry as piano factory.

- [S4757] Edwin N. Shurtz, Return of Births in County of St. Joseph.

- [S4839] Alice L. Morse household, 1900 U.S. Census, Cook Co., Illinois, shows name as Edwin Shurtz.

- [S4838] H M Cable household, 1910 U.S. Census, Cook Co., Illinois, shows name as E. W. Shurtz.

- [S4842] Bumstead's La Porte City and Business Directory, 1910-1911 pg 234, shows name as Edwin W. Schurtz.

- [S4843] Smith's Directory of La Porte, Ind., 1913 pg 234, shows name as Edwin W. Shurtz.

- [S4816] "Society Leaders Killed," Hamilton Evening Journal, 21 Oct 1913, shows make of car.

- [S4814] "4 Die in Auto Crash," The Washington Post, 19 Oct 1913.

- [S890] "Indiana WPA Death Index, 1882-1920," Ancestry.com, record for Mary Edith Schurz, citing bk H-28 pg 87 by Indiana WPA, shows date and county.

- [S4843] Smith's Directory of La Porte, Ind., 1929-30 pp 85, 205, 246.

- [S4833] Charles M. Newline household, 1930 U.S. Census, La Porte Co., Indiana, shows occupation as controller, industry as piston manufacturer.

- [S4845] La Porte Indiana ConSurvey Directory, 1938 pp 239, 354.

- [S12882] Edwen Williard Schurz, Certificate of Death, shows occupation as executive, industry as factory office.

- [S4810] Edwin Schurz household, 1930 U.S. Census, La Porte Co., Indiana.

- [S4845] La Porte Indiana ConSurvey Directory, 1929-30 pg 354.

Wilmer A. Shurtz1,2,3

#18976, (1876 - 1906)

Parents

| Father | Frederick J. Shurtz (1832 - 18 May 1892) |

| Mother | Sarah Elizabeth Riegel (20 Mar 1842 - 27 Nov 1920) |

| Ancestry | The Reigel Family |

| Chart Membership | Descendants of Jacob K. and Christiana Ohl Riegel |

| Family Indexes | The Reigel Family |

Key Events:

Marriage: 10 Sep 1897, Imogene, Fremont Co., Iowa, Cora J. Arnold (b. 2 Feb 1880, d. 25 Jan 1909)7,8,9

Burial: 8 Sep 1906, Shenandoah, Page Co., Iowa,13

Copyright Notice

The material on this website is subject to copyright.